Joby Aviation (JOBY): “Uber Meets Tesla In The Sky” Is Set To Crash And Burn

Introduction

By 2024 the FAA will approve a new style of aircraft. It’s electric, and takes off and lands vertically, an “eVTOL.” These will immediately begin commercial operations as an “air taxi” service. By 2026, one company claims it will have manufactured 963 of these aircraft and the air taxi service it will operate will generate $2.2 billion in revenue. Its vision is to save a billion people an hour a day, a claim so grandiose it is hard to fathom.

Currently with no revenue, one prototype plane, and promises of the future, Joby Aviation (NYSE:JOBY) has some of the most egregious guidance of any SPAC we have seen. The implications are enormous: Joby claims it will produce more aircraft than the largest aircraft manufacturers today. It will then operate an air taxi service with 9 times more daily departures than Delta.

These claims have helped Joby achieve partnerships with Toyota and Uber, eventually going public in a $4.5 billion SPAC merger in August 2021. Joby has styled itself as the leader in the race to get eVTOLs into the sky. It has benefited from the most funding and has flown its pre-production prototype aircrafts the most, the farthest, and the fastest. Unfortunately, as much as we hate traffic, we believe Joby has severely overstated what it can do.

Currently worth $3 billion, we think Joby is built on a tangled web of inconsistencies and promises that are impossible to achieve. We believe Joby is publicly overstating how many planes it can produce, and we think it has misconstrued its unit economics. We believe the project will be massively delayed and miss timelines by years. We are not alone in this belief; Joby’s management concurs.

We are short shares of Joby. Please read the full disclaimer at the end of this article.

We Believe Joby Is Publicly Overstating How Many Airplanes It Plans To Make

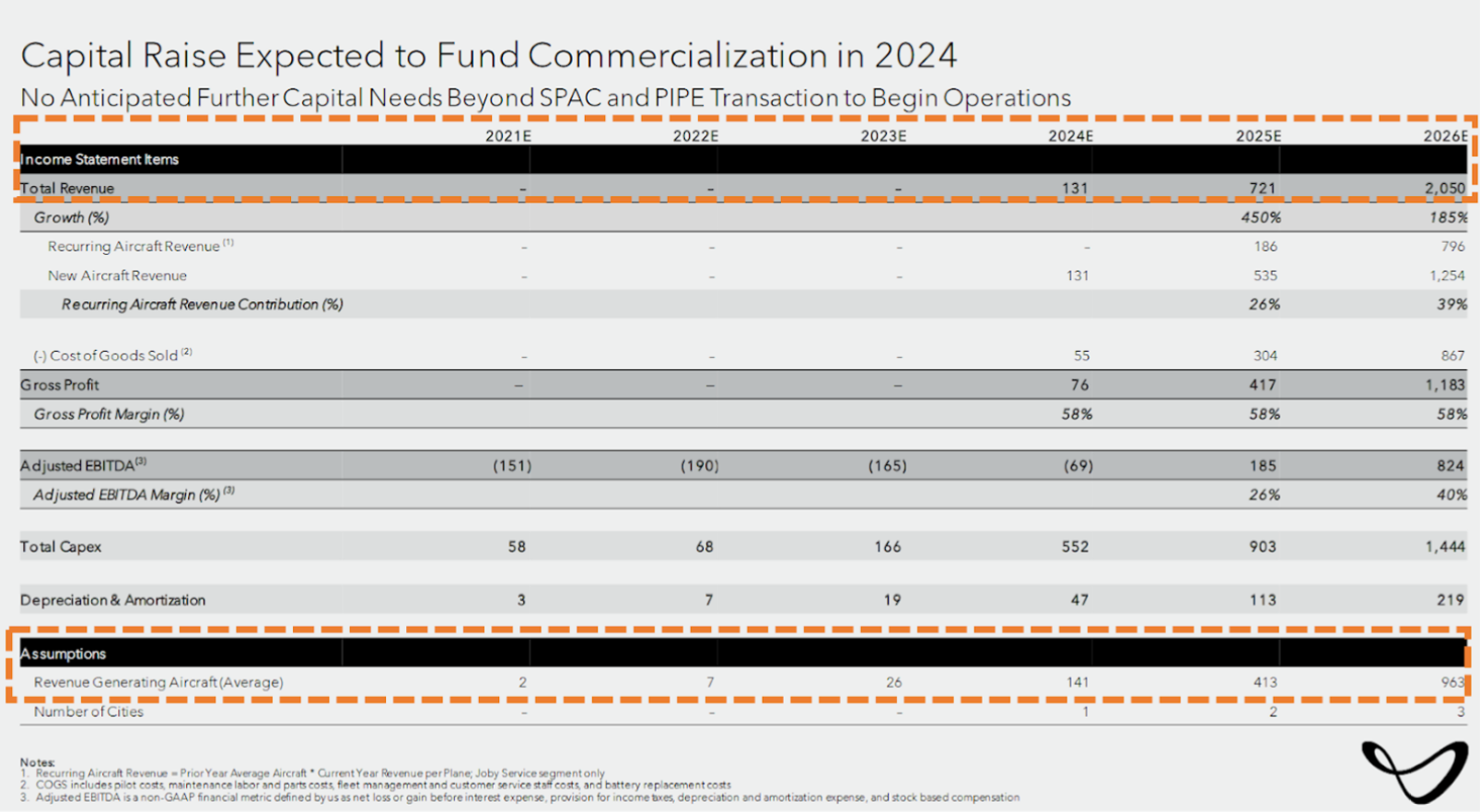

Joby claims to investors that it will build 141 aircraft by 2024, generating $131 million in revenue that year. By 2026, it will have built 963 planes, and claims it will generate over $2 billion in revenue.

Source: Joby Investor Presentation

Joby is building its manufacturing facility at the Marina Municipal Airport near Monterey, California. Joby tells investors it will soon have many aircraft coming off the production line. However, local government files obtained through a public records request show that Joby seems to have massively overstated its production plans to investors.

According to a government produced engineering evaluation, Joby is telling local authorities that its initial plan “is to build up to 10 planes per year in the next couple of years, and up to 30 planes in about 5-7 years.” Joby has told investors it will manufacture over 100 planes in 2024.

Source: Joby Engineering Evaluation

Understanding The Scale Of What Joby Promises

We think the guidance Joby has provided to local authorities is much more reasonable than what it has told investors. The scale implied by Joby’s manufacturing plans is massive. Joby is telling investors that it will become the largest aircraft manufacturer in the world by 2026.

Joby’s Manufacturing Guidance:

Source: Joby Investor Presentation, Page 31

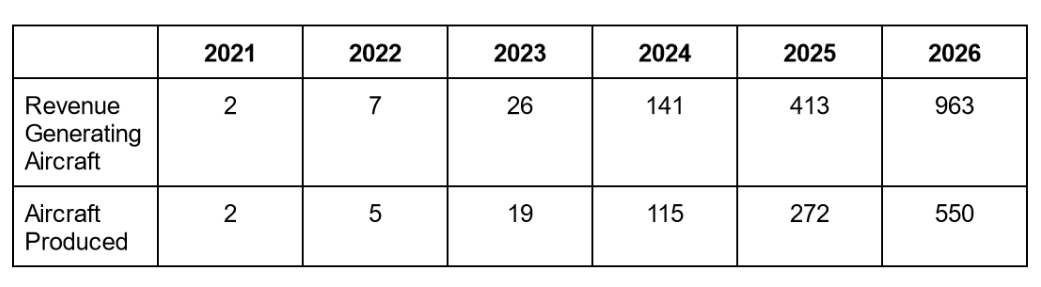

Joby claims that by 2026 it will have 963 aircraft producing revenue. Yearly aircraft production numbers will go from 19 in 2023 to 550 by 2026.

Not stopping there, Joby’s long-term plans call for 14,000 aircraft generating $20 billion a year in revenue by 2031. This is more than double the number of aircraft that Boeing has built over the last ten years.

Source: Company filings

For additional context the most widely produced civilian helicopter in recent memory was the Bell 206 JetRanger. 8,460 of these aircraft were produced between 1966 and 2010. They didn’t even have an air taxi service to operate!

For even more context, there are around 10,000 helicopters in the United States right now. Just to put Joby’s long term targets of 14,000 aircraft into perspective. Boeing has built about 6,405 airplanes in the last ten years. Joby is claiming it can manufacture these planes, starting from scratch, and do so by spending much less money than other competitors.

Joby claims that it will not need to raise any more capital to get to commercialization. It claims that by 2026 its total capital expenditures will be $1.4 billion (not yearly), a tiny fraction of the yearly capex of major airline operators and aircraft manufacturers. If Joby is years away from generating revenue and capex projections are low, we believe Joby will need significant dilutive capital raises to even get the business going.

The scale of what Joby claims to be doing dwarfs both the manufacturing and operations of aircraft manufacturers and U.S. airlines, yet it plans on achieving this by spending far less.

Source: Bloomberg, Company Filings, Joby Investor Presentation

Joby will not only be manufacturing aircraft, it will also be operating an air taxi service. Joby will somehow be able to do this while spending only a tiny fraction of what other airlines and aircraft manufacturers spend on annual capex.

Joby’s Vision and Operational Plans: The Math Ain’t Mathin

As a vertically integrated company, Joby makes both ridiculous manufacturing and ridiculous operational plans. According to its own guidance, its air taxi service will dwarf the size of the largest airlines today and implies a doubling of total air traffic in the United States.

Joby’s vision is to “build a global passenger service that saves a billion people an hour every day.” This is the very first thing it tells us about itself in SEC filings, and they have repeated it in ongoing investor presentations. Our view is that Joby is playing it fast and loose with math, and we think this is a good example of how.

If Joby can build 963 aircraft by 2026, and they are taking off 40 times per day, that translates into roughly 14 million flights per year. Last year, the FAA supervised 16.4 million flights in the U.S. Joby’s guidance is so aggressive that it implies a near doubling in the amount of aircraft taking off in the United States on a daily basis.

But to impact a billion people? It would require 13,000 aircraft making 40 trips per day. Joby tells us it will carry an average of 2.3 passengers per flight. To impact 1 billion people a day, they would need 10.8 million aircraft. Joby currently has ONE PLANE that is a prototype, yet their guidance implies it will be operating an air taxi service as large as the total number of commercial flights that occur in the U.S annually.

Joby’s guidance claims it will be charging $3 per seat per mile. It claims an average flight length of 24 miles, which means that a ticket on a Joby would cost around $70. While Blade (BLDE) is not a direct competitor, it offers a similar service.

Blade’s short distance flights can be purchased as low as $95 with a membership (normal rates start at $195). In Blade’s 2021 fiscal year, 27,665 seats were purchased on all of its flights. Joby’s guidance suggests that it will be making 38,500 DAILY FLIGHTS, carrying an average of 2.3 passengers per departure. Delta flies about 4,000 flights per day.

Joby’s Manufacturing Plans Seem Behind Schedule, And Progress Seems Slow

Joby has been working on manufacturing plans with the air resources district since 2020. In January 2020, Joby presented a master site plan to the Marina City Council. Joby projected that within 15 months (Q2 of 2021), Joby would have half of the mass production factory built and ready to operate.

30 months later, only the basic structure of a pilot production tent has been erected. The 200,000 square foot projected Phase 1 factory is nowhere to be seen.

In February 2022, Joby submitted a building permit application for a 1,500 square foot freestanding paint booth for the pilot production tent to the city council. The permitting office has required multiple revisions to the application, and seven months later, this extremely simple facility remains pending approval.

We believe Joby has backed itself into a timeline that is untenable, and that soon it will have to come clean that it is behind pace, and begin to push its timeline out.

Source: Joby Aviation Manufacturing Facility Initial Study, prepared by City of Marina

As of June 2022, the only thing built was a large tent on the location where the manufacturing facility will be located. Joby reduced their spending guidance on the Q2 earning call, but we think this is simply because the building of the plant is not happening at the expected cadence. We think this will soon translate into pushed back timelines, and lower revenue guidance.

Source: Engineering Evaluation Report

Joby is already behind schedule on some claims. In June 2021, Joby hosted an analyst day, where it claimed it would be announcing its launch markets in the second half of 2021. We are entering Q4 of 2022, and no launch markets have been announced.

Joby Commercialization Timeline And FAA Approval Concerns: Joby is delivering a much more aggressive tone than competitors

When 60 Minutes did a piece on the eVTOL space in April, they highlighted Joby and several competitors. Wisk, led by Gary Gysin, is working on a similar project, albeit trying to create an autonomous eVTOL. Wisk is targeting a launch “in the next decade.”

When Gysin was asked by Anderson Cooper about not giving a date as to when they think they will be operational, he responded by saying:

“Yeah, you know why we don’t do that? Because we’re not in control of that part. The FAA is. In Europe, it’s called EASA. They’re in charge. So when they certify aircraft to fly, that’s when you fly.”

When Anderson Cooper asked Joby CEO JoeBen Bevirt a similar question, he responded much differently.

Anderson Cooper: “How far are you from getting the first Joby in the sky with passengers”

Joeben Bevirt: “So we are launching our service in 2024.”

Anderson Cooper: “You think you can do it that quickly?”

Joeben Bevirt: “Yes.”

We think it is EXTREMELY unlikely that Joby is able to launch commercial operations in 2024.

“We believe mass eVTOL deployments in the early-to-mid 2020s are unlikely given large technological, regulatory, and infrastructure-related hurdles” - Asad Hussain, Pitchbook 2021

Even industry proponents think Joby’s timeline is aggressive. The Revolution.Aero conference brought together many eVTOL leaders in early September. JP Morgan summed up the general view on timelines by saying:

“Some panels discussed the initial passenger use case around 2025 in very small scale, with ‘widespread adoption’ across multiple cities not likely within this decade, but more likely in ~10 years (2030-2035 time-frame).

Much like Joby’s manufacturing and operational assumptions, we think Joby has been far too aggressive in laying out its approval timeline. The FAA has never approved a tilt-rotor design like Joby’s. The closest comparison we could find is the Leonardo AW609, which is finally nearing FAA certification two decades after its first test flight.

Joby Crashes In February: Company Plays It Down, Might Cause A Huge FAA Issue

On February 16, 2022, Joby was flight testing one of its prototype aircraft. Operating at speeds much higher than top speeds, the Joby aircraft had what the NTSB described as a “component failure.” Joby’s CEO called it an “envelope pushing” flight, and the company downplayed the issue. To be fair, you want these crashes to happen in testing and not when it is operating with passengers.

However, these kinds of flights are required by the FAA, and flying an aircraft above max speed is part of the FAA approval process. According to Aero News, Joby needs to demonstrate that it can fly its aircraft at speeds 1.3x its stated top speed as part of the FAA approval process.

The crash left Joby with only one eVTOL for testing. It paused testing after the flight and restarted it several months later. Just a year ago, Joby said it would have 7 revenue generating aircraft this year, and they have none, not to mention just one remaining prototype - highlighting the fragility of their extremely aggressive timeline.

Joby Tweets Video Of Their Plane Flying “Ongoing Testing”

In July, Joby tweeted a minute long video of a Joby in flight undergoing “ongoing testing,” highlighting that it had intentions of bringing Joby to the UK market.

The video showed a Joby with the tail number N542AJ in various stages of flight. This video could not have come from ongoing flight testing like Joby says, as Joby N542AJ crashed in California in February.

Source: Joby Twitter

Joby’s Current Certification Is Underwhelming

Source: Bloomberg

Between February 15 (the day before the crash) and March 14, Joby’s shares would fall almost 30%. Joby then released a spate of press releases touting advancements in its FAA certification process.

Source: Joby Investor Relations

These press releases helped the stock rise 60% through the second half of March. One could be forgiven for seeing these headlines and thinking that Joby was nearing FAA approval. On May 26, Joby announced that it had received Part 135 Certification from the FAA.

“ Certification allows Joby to operate commercially.”

What Joby is certified to operate commercially:

A Cirrus Sr22, Source: AerospaceAmerica

Joby received the certificate from the FAA to operate conventional aircraft. In this case, they own a couple of small regular planes, which Joby says will help them refine systems and procedures prior to launching the eVTOL service in 2024.

What Will Joby’s Operations Look Like?

Joby will be operating under a Part 135 certification as an operator that provides private air charter or air taxi services, importantly letting Joby’s fly with only one pilot. Joby’s unit economics would massively deteriorate if it needed two pilots.

Joby will operate a fleet of vertiports in the cities that it operates in, and current indications suggest that it will put these on top of parking garages. So passengers will have to drive to a parking garage, park, and then fly across town, presumably needing to fly back to get to their car.

Joby’s model has it operating a massive network of flights in the most crowded cities and airspace in the world. This is highly regulated airspace. New York banned building heliports on top of buildings after a helicopter crashed landing on the Pan Am Building in 1977, killing 5 people. Currently, there are only three heliports in NYC.

Joby’s Long-Term Vision Implies Plane Revenue Will Drop Off Massively—Joby Has Never Addressed This

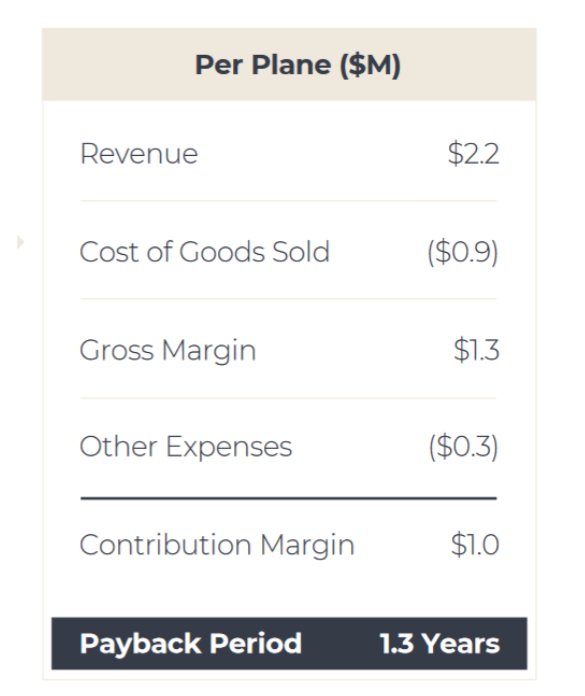

Joby claims that by 2026, it will have 963 aircraft that generate $2.05 billion in revenue. Joby’s investor presentation claims $2.2 million in revenue per plane at scale.

Source: Joby Analyst Day, Page 85

Yet under Joby’s own long-term guidance, the revenue per plane will drop 33% from $2.1 million to $1.4 million per plane if it has 14,000 planes doing $20 billion in revenue.

Source: Joby analyst day, math

Joby has never addressed this. It strikes us as further evidence that Joby has not thought much about the implications of the numbers and guidance it has given investors.

Joby’s filings indicate that “since our inception in 2009 we have been primarily engaged in research and development of eVTOL aircraft.” This isn’t entirely true.

Joby claims it has been working on an eVTOL since its inception in 2009, this isn’t entirely true. Joby’s first idea was an airborne wind turbine.

Source: JobyEnergy.com via Wayback Machine

A 240 foot long wing would be tied to the ground and raised 35,000 feet into the air. At that height it could capture the energy of the jetstream, sending clean energy back down to the ground through the winch.

At the time, JoeBen said the project would be off the ground in about 3 years at a cost of $100 million. But the project ran into issues with the FAA (remember history doesn’t repeat but it does rhyme).

“The firm originally wanted to float turbines in the jetstream but the FAA was less than happy about that. According to the CEO, “The clear message from the FAA is we don’t know what to do with this at 35,000 feet.”

According to at least one article at that time, the company started working on eVTOLs as it was so impressed with the turbine they developed, it began to work on a personal aircraft.

JoeBen was able to fund the early development of the company thanks to several successful exits. He started his first company Velocity 11 in 1999 and sold it to Agilent in 2007 for $100 million. In 2006 he introduced a successful series of flexible camera tripods called Gorillapods, sold by a company also called Joby.

Joby’s Similarities To A Long String Of Failed Aviation “Next Big Things”

We see many similarities between Joby and other “next big things” in aircraft manufacturing. Notably extremely aggressive FAA approval timelines, extremely aggressive manufacturing guidance, and ambitious long-term goals.

The Original Flying Car

JoeBen Bevirt may have gotten the idea for his eVTOL from his time in college, where he worked in a lab run by Dr. Paul Moller at UC Davis. Dr. Moller has been working on a flying car for over 50 years. He is well-regarded in the aviation industry, despite the challenges his project has encountered.

JoeBen has spoken highly of Dr. Moller, and a 2011 Discover Magazine profile of the inventor while Joby was still working on flying turbines.

“It was at the University of California, Davis, that Bevirt found his calling, in one of the most peculiar laboratories in the state. “Paul Moller is this totally crazy inventor in Davis who has been working for the past 40 or 50 years to build a flying car,” Bevirt says, smiling broadly at the memory of his mentor. “It was an amazing experience.” From his sophomore through his senior years, Bevirt worked all hours alongside Moller and a few other engineers trying to figure out a controlled way to lift a vehicle and its driver off the ground.”

Paul Moller has been trying to build a flying car for over 50 years. Over that time he says he has raised $100 million dollars to build prototypes, a fraction of what Joby has raised. Moller doesn’t seem to think too highly of his competition, saying:

As the story noted:

“Moller keeps a close eye on the eVTOL landscape and writes extensive reports comparing different companies. He keeps the findings to himself, though, not wanting to hurt what he sees as the inevitable end to eVTOL companies - including Joby Aviation…If he’s [JoeBen Bevirt] going to self-destruct, I’ll let him do that.”- Paul Moller

And he doesn’t think very much of his current competition and seems to think the FAA will hold the process up.

“Anything that’s really different from what is conventionally being processed by the FAA is going to have a very indeterminate timeline for completion. My view is that the eVTOL market is going to self-destruct in the coming year.”

Source: Paul Moller via Freedom Motors

Similarities To Joby

In 2001 Moller International went public, its filings not reading that different from Joby’s current filings. Indeed a brochure advertising the Skycar claimed that it would be introducing vertiports to handle the takeoff and landing of the craft, just like Joby.

At the time of the IPO they had minimal commercial operations, but claimed that in just a couple of years they would be selling their Moller Skycar for less than $1 million. Ironically they also noted a minimal noise impact. What’s old is new again. Moller even pitched a military angle, just like Joby!

But the SEC had something to say about some of the promises Moller made to raise money, bringing charges against Moller and the company in February 2003, in part due to Moller’s misleading claims and statements made in efforts to raise money. (History doesn’t repeat but it rhymes).

“The promotional material used in this solicitation campaign contained materially false and misleading information. For example, the Skycar, according to Moller, would allow any person to travel at speeds over 400 miles per hour in the uncluttered airspace about the roadways for about the same price as a luxury automobile. In [Moller International] investor newsletters, Moller projected that 10,000 Skycars would be sold by the end of 2002.” - SEC Litigation

Moller would settle without admitting guilt. Moller is still at it, well into his 80s.

Conclusion

Joby is a pre-revenue company that we believe is a long way away from having commercial operations. We believe it has overstated to investors its production capabilities and timeline. We don’t see a path to near-term FAA approval. We think the company has played it fast and loose with math and the implications of the numbers it has put into its guidance.

There is a long history of “the next big thing” in aviation, and not many have ended well. We hate traffic, and would love to see a service like this in operation, but we do not think Joby can do what it has told investors it can do. We are short shares of Joby, and expect it to collapse over the next several years crushed by longer than expected approval timeline and smaller manufacturing operations than it has conveyed to investors.

Disclaimer:

By downloading from or viewing material on this website you agree to the following Terms of Service. Use of Bleecker Street Research LLC’s research is at your own risk. In no event should Bleecker Street Research LLC or any Bleecker Street Research LLC Related Person (as defined hereunder) be liable for any direct or indirect trading losses caused by any information on this site. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities of an issuer covered herein (a “Covered Issuer”).

As of the publication date of Bleecker Street Research LLC’S report, Bleecker Street Research LLC Related Persons (along with or through its members, partners, affiliates, employees, and/or Bleecker Street Research LLCs), clients, and investors, and/or their clients and investors have a short position in the securities of a Covered Issuer (and options, swaps, and other derivatives related to these securities), and therefore will realize significant gains in the event that the prices of a Covered Issuer’s securities decline. Bleecker Street Research LLC and Bleecker Street Research LLC Related Persons are likely to continue to transact in Covered Issuers’ securities for an indefinite period after an initial report on a Covered Issuer, and such position(s) may be long, short, or neutral at any time hereafter regardless of their initial position(s) and views as stated in the Bleecker Street Research LLC’S research. One or more Bleecker Street Research LLC Related Persons have provided Bleecker Street Research LLC with publicly available information that Bleecker Street Research LLC has included in this report, following Bleecker Street Research LLC’S independent due diligence.

Research is not investment advice nor a recommendation or solicitation to buy securities. To the best of Bleecker Street Research LLC’s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the securities of a Covered Issuer or who may otherwise owe any fiduciary duty or duty of confidentiality to the Covered Issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Bleecker Street Research LLC makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Research may contain forward-looking statements, estimates, projections, and opinions with respect to among other things, certain accounting, legal, and regulatory issues the issuer faces and the potential impact of those issues on its future business, financial condition, and results of operations, as well as more generally, the issuer’s anticipated operating performance, access to capital markets, market conditions, assets, and liabilities. Such statements, estimates, projections, and opinions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Bleecker Street Research LLC’s control. All expressions of opinion are subject to change without notice, and Bleecker Street Research LLC does not undertake to update or supplement this report or any of the information contained herein. You agree that the information on this website is copyrighted, and you, therefore, agree not to distribute this information (whether the downloaded file, copies/images/reproductions, or the link to these files) in any manner other than by providing the following link: Bleecker Street Research LLC bleeckerstreetresearch.com The failure of Bleecker Street Research LLC to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to the use of this website or the material herein must be filed within one (1) year after such claim or cause of action arose or be forever barred.

Bleecker Street Research LLC Related Person is defined as: Bleecker Street Research LLC and its affiliates and related parties, including, but not limited to, any principals, officers, directors, employees, members, clients, investors, Bleecker Street Research LLCs, and agents.